End of Cheap Energy and Peak Debt Levels Presage Collapse

The huge increase in world population in the past 150 years, the food production to feed those people and the rise of modern specialized society was based on cheap energy, technology and the rise of debt (capital). But the most important thing is energy. In a way, energy is everything. Coal, then oil fueled the industrial revolution and the rapid growth up to 2008. Raw materials, including coal and oil, were very cheap until recent decades.

Cheap oil energy is no longer available for additional barrels demanded. Oil is available but it's not cheap! If oil prices shoot up to over $100 or more when extra barrels are demanded like in 2008, or in response to Chinese demand in 2009/2010, then we've reached the end of cheap oil. Remember, world GDP growth and energy consumption go hand in hand.

We're also reaching the end of debt's marginal utility, meaning the amount of growth per unit of debt has declined to nearly nothing. I call it "debt saturation." Here's the point of this blog post: if we've reached the end of affordable energy and debt's marginal utility, then we've reached the "end" of world GDP growth. And if strong GDP growth is ending, then the debt "edifice" built up to fund recent year's growth may prove to be unsustainable. In fact, the debt crisis in 2008 is likely to be a prelude to more debt trouble -- even massive defaults -- in the years ahead.

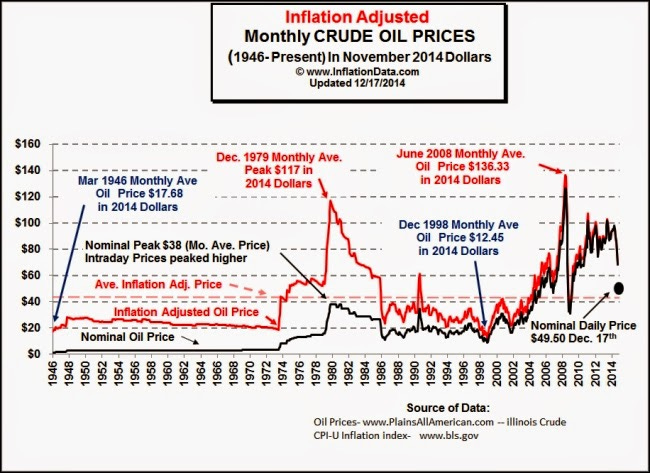

In the interest of brevity, I don't want to recap recent world history, but instead focus on recent years. When oil prices hit $145 in 2007/2008, it caused a recession and triggered financial crisis in the US and the world. It's entirely possible that $108 oil in 2014 has triggered another recession in 2015--coupled with the fact that China has cut back it's credit-fueled growth (due to the declining utility of debt there). Further below, I explain why China can no longer ride to the world's rescue.

The financial crisis in 2008 was due to high oil prices and also the high indebtedness of US consumers. Consumer debt reached a peak relative to incomes, mostly due to mortgages (debt saturation). High oil prices hurt the economy, left consumers with less discretionary income and many couldn't pay all of their bills including mortgages. The mortgage and housing markets collapsed which then threatened the solvency of banks -- and the entire financial system. So, the cost of oil triggered a sudden economic recession in 2008 like in 1974 and 1981 (see chart above). Financial institutions around the world also faced a panic and world trade ground to a temporary halt as Letters of Credit were refused or unavailable. It was a near-death experience. In summary, you could say that world consumers reached a limit in indebtedness due primarily to the cost of energy. Consumers couldn't bear the cost of energy and debt collapsed.

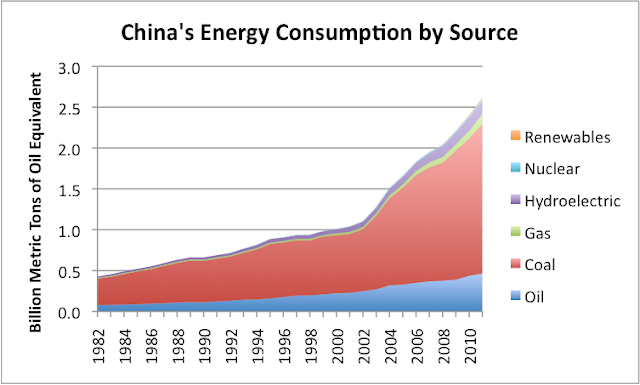

In response, the US started it's money "printing" program, countless other programs, and huge deficit spending. China panicked and embarked on the most amazing debt-fueled spending ever seen in world history. In 5 years, China's ratio of credit to GDP has jumped by 75 percentage points to 200pc of GDP or more. How did China do that? They embarked on debt-financed programs to build ghost cities, still-empty malls, millions of units of housing in still-unoccupied buildings. To do this, they needed huge amounts of energy, raw materials and debt. Since world oil production is mostly limited (any extra demand causes oil prices to spike to unaffordable levels), China used mostly cheap domestic coal to fuel their breakneck expansion. China used huge amounts of coal since 2009.

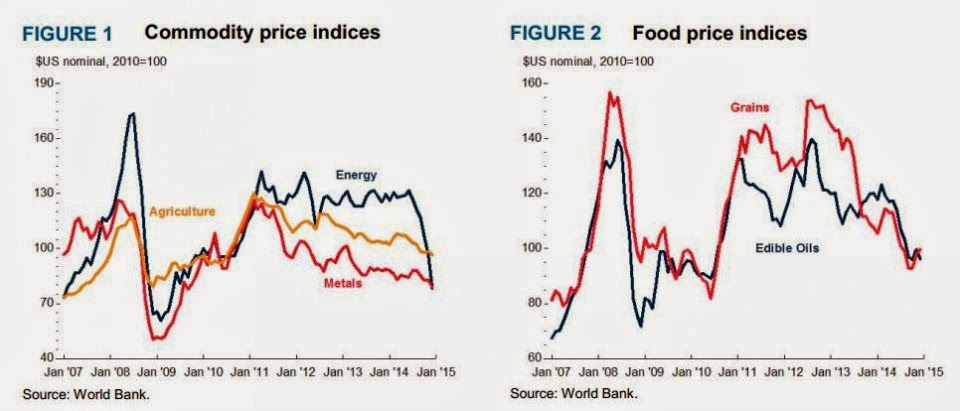

Now even China has reached an indebtedness that is highly correlated with financial crises. Even they realize it and have recently scaled back on new credit growth -- causing their economy to slow. China's reduction of debt increases and slowdown has caused key world commodity prices to crash with iron ore, copper and oil down by more than 50% since 2011. Debt growth only slowed there -- it's not declining! Even slowing debt growth causes commodity prices to collapse!

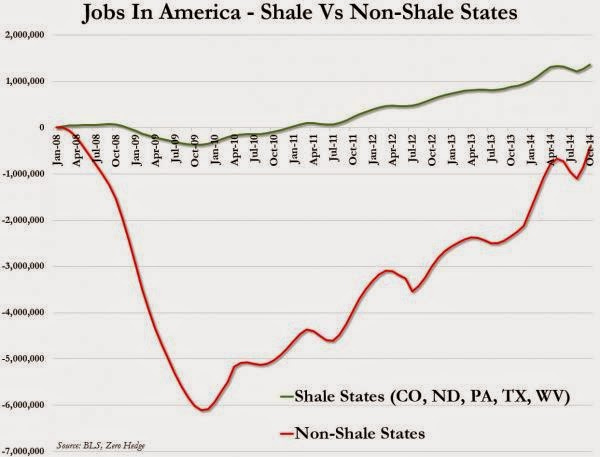

In the US, in the past 3 years, the shale oil and gas boom increased US oil production by 3 million barrels per day (while the rest of the world's production has been flat to slightly down). When China started to slow it's debt-fueled expansion, it caused reduced total oil demand by them and commodity-producing countries, and accounts for the big plunge in oil (and other commodity) prices worldwide. The boom in US oil and gas production was largely responsible for nearly all of the high-paying employment growth in the US since the 2008 financial crisis. Now that boom is likely over. Employment will fall in the US unless oil prices rise quickly. Falling employment means recession.

If Shale Boom Is Over, Then Employment in US Will Drop. Dropping Employment Signify Contraction or RecessionYou might say that cheaper oil will give the world economy room to grow. It's true that some oil importing countries will be helped. But the plunge in commodity prices is hurting all of the commodity exporting countries, ie., the Middle Eastern countries, Brazil, Russia, Venezuela, Canada, Australia and many other countries in Africa and Latin America. These countries will likely be in recession and their demand for US exports will drop. This effect has recently shown up in declining US export data.

Even the long-term future of the shale oil boom is threatened since it was funded by cheap debt which will no longer be cheap enough for many of the companies. Credit for marginal shale producers may not be available at all. Remember that shale oil and oil sands are the only worldwide sources of marginal production in recent years and were only made possible by extremely high oil prices. If loans to shale drilling companies is not available, it may mean that oil spikes will be even higher in the future should demand "try" to rise. In the next few years, this may mean that we will see even larger oscillations in oil prices and, therefore, instability in the economy. This is an effect of "hitting the wall"-- or hitting the limits of resources and growth.

More immediately, reduced demand for US exports from much of the world, reduced employment in the oil patch in the US (the only bright spot in the US economy) may trigger a recession in the US since growth has only been running at about 2%. It's entirely possible that it's already showing up. For example, the past two month's retail sales were down sharply (some of that is due to lower gasoline prices). US exports and durable goods orders were down sharply for the past two months as well. China is slowing very sharply. Europe is basically already in recession. Evidence of world recession is mounting. Brazil and Russia are likely in recession. Debt defaults may be imminent for Venezuela, Russia and other countries. These defaults and recessions may trigger further financial crises, with massive losses for investors in equities which will further reinforce the recessionary forces.

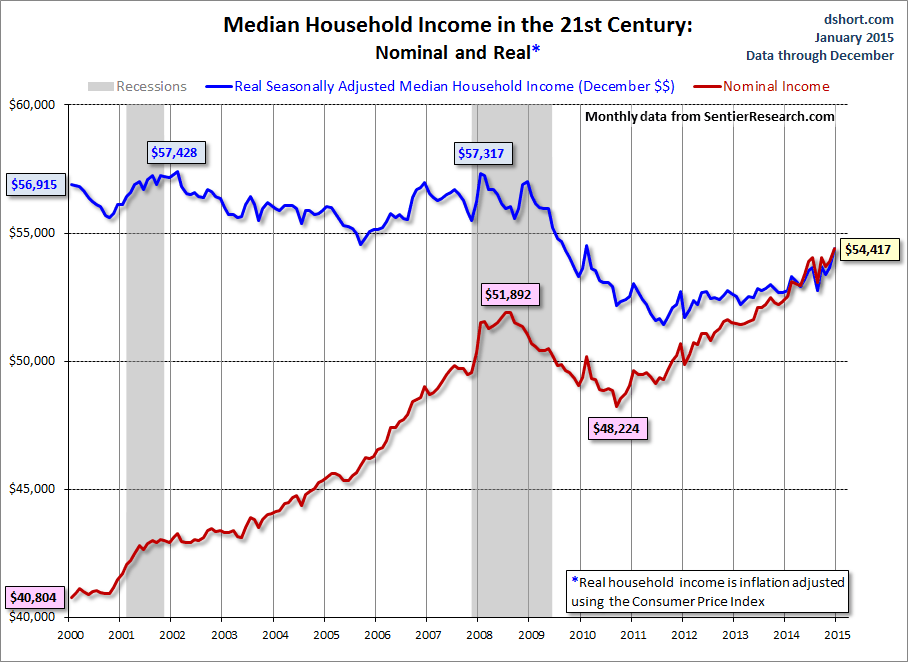

Since 2009, real median incomes are down for the US (see graph below) and the reduced employment in the oil patch will further reduce it. Thanks to Obamacare, consumers are under pressure from much higher healthcare insurance costs and are not able to spend the money saved at the gas pump. Food prices and rent prices have also become big burdens for consumers since their incomes are mostly stagnate to falling.

The debt carrying capacity of consumers falls as income falls. And due to the rising cost of non-performing loans, some consumer interest rates will go up for such loans. Small shale oil company's cost of credit will go up or dry up. Interest rates for highly indebted companies will go up as Junk bond interest rates rise (this is already begun). Recession will aggravate this situation. Defaults will rise and marginal credit interest rates will rise. The debt carrying capacity for entire countries like Venezuela, Argentina and even Russia is now in doubt.

Debt levels are at dangerous levels everywhere now. Slowing growth in economies makes the burden of debt more difficult for corporations and governments. Eventually even government debt levels may become a problem. US debt levels have risen 80% to $18 Trillion in the past 6 1/2 year alone with shockingly little effect! Clearly this trajectory is unsustainable.

Perhaps more ominously, if the world economy tumbles back in recession, then the entire world is ill-prepared to offset an economic downturn. Other than rising government deficits, there are few effective counter-cyclical policy tools available. Interest rates are already zero here and in most places. Money printing has been discontinued in the US as it's continued use has been proven to be ineffective. As I've mentioned, there's evidence that even increased government deficit spending no longer boosts GDP as much as in the past -- the collapse of debt's marginal utility worldwide.

China has reached dangerous levels of debt due to it's vast and desperate investment program on largely uneconomic projects. It's difficult to see them re-initiating such a program. Their housing projects and ghost cities are still empty. There are other limits as well. For example, China was recently consuming up to 60% of the world's coal, iron ore and copper. If China wanted to maintain 7% growth rates like the past, then their demand for such raw materials would double in 10 years along with their economy -- this means that in 10 years, demand for commodities would exceed 100% of the world's supply of nearly everything! The cost of those materials would sky rocket! As mentioned before oil prices would spike dangerously and unsustainably higher! Their coal use would have to double as well at a huge cost. Even now, air and water pollution are a serious and real threat to the population in China. People can barely breath there today. You can see how they've reached a limit to their growth rate. The same effect applies everywhere else! There are limits to growth in a world of limited low-cost energy and resources!

And debt loads built up worldwide, especially after the 2008 crisis, may very well prove to be unsustainable at some point as growth permanently stalls. Eventually, confidence could evaporate or, if money printing is re-established everywhere to monetize government debt issuance, then inflation may create the next crisis in market interest rates and markets in general.

If I say to anyone these days "everything is falling apart" I get nods of agreement. It's possible that recession, debt crises, depression, social unrest and war lie in our future. Even now, war has broken out in E. Europe and the Middle East is in flames. China is threatening neighbors in SE Asia. Some of these conflicts are due to desperation of regimes to divert the public attention and boost nationalism at home (Russia and China). And seven years after the 2008 meltdown, the US (and world economies) are still on life support. Still-rising government debt is barely keep economic growth in positive numbers. Zero interest rates, vastly expanded money supply, still high fiscal deficits, $8 trillion in new US gov't debt (and growing) haven't worked well except to bide time. Therefore, no policy tools remain to counteract the next downturn. We're just one economic shock away from the next recession. And with no effective policy tools remaining, the next Great Depression may be around the corner.